REVIEW

of

FINANCE -

November, 2018

55

of strongest effect to achievement of goals and

most effective use of resources. Cost accounting

also helps managers quantify the plans by

means of making budget statements including

consolidated budget and detailed budgets for

divisions, activities or products. In these budget

statements, cost information must be used since

there is no cost information there is no budget, and

it is impossible to allocate resources to implement

plans as well as there is no instrument to measure

the operation results or evaluate the achievement

of strategic goals.

Organizing:

Organizing means combining

activities and linking factors such as organization,

labour and resources to implement and achieve

a plan. When organizing a plan, managers need

frequent information of costs to seize the situation

of resource utilization for the activities of divisions,

thereby; they are able to evaluate plan progress.

Cost information helps them discover the real

inadequacies of divisions, phases or areas of

business; hence, they are able to take appropriate

and timely measures to reallocate resources

more effectively or to coordinate with internal

and external divisions more closely. Particularly,

when organizing a plan in the context of volatile

environment, managers have to conduct frequent

evaluation on the aspects of resource utilization

and operation performance under different

situations. Therefore, they need cost information

for every situation to determine the best options

in terms of costs.

Controlling:

Controlling is the process of

supervising, measuring, evaluating and adjusting

activities to ensure plan progress. On one hand,

controlling is an instrument that managers employ

to discover inadequacies and apply measures. By

controlling, on the other hand, activities will be

smoothly implemented and faced fewer risks.

Controlling is not the final step in management; it

is a continuous process in terms of time and space.

Controlling is a system responding to operation

results and forecasts as well. The response system

of results helps establish standards, estimate

outputs and adjust variation. To implement

adjustment, managers apply an adjustment

program and run it to achieve expected results.

The response system of forecasts helps monitoring

inputs and implementation process to make sure

whether they are stable and reliable, this system

also enables response to be implemented prior

to the system outputs. An effective controlling

system must be a combination of final output

control and forecast control. To maximize the

efficiency of resource utilization, costs should be

controlled by both systems in all phases of pre-

plan implementing (designing phase), during

plan implementing (input supply, production

and sale) and post-plan

implementing to draw lessons

for the next periods.

+ Controlling costs before

implementing plan (designing

phase), this phase considerably

impacts the production results

which involves selection of

materials, technology and costs

of the value chain and supply

chain. The major proportion of

costs for a product life-cycle

is determined in designing

phase. To well-manage costs

in designing phase, managers

need cost estimation for each

activity, phase or product item.

Product is the result of activities

and aggregation of consumed

costs into those activities,

DEVELOPING MANAGEMENT ACCOUNTING IN ENTERPRISES

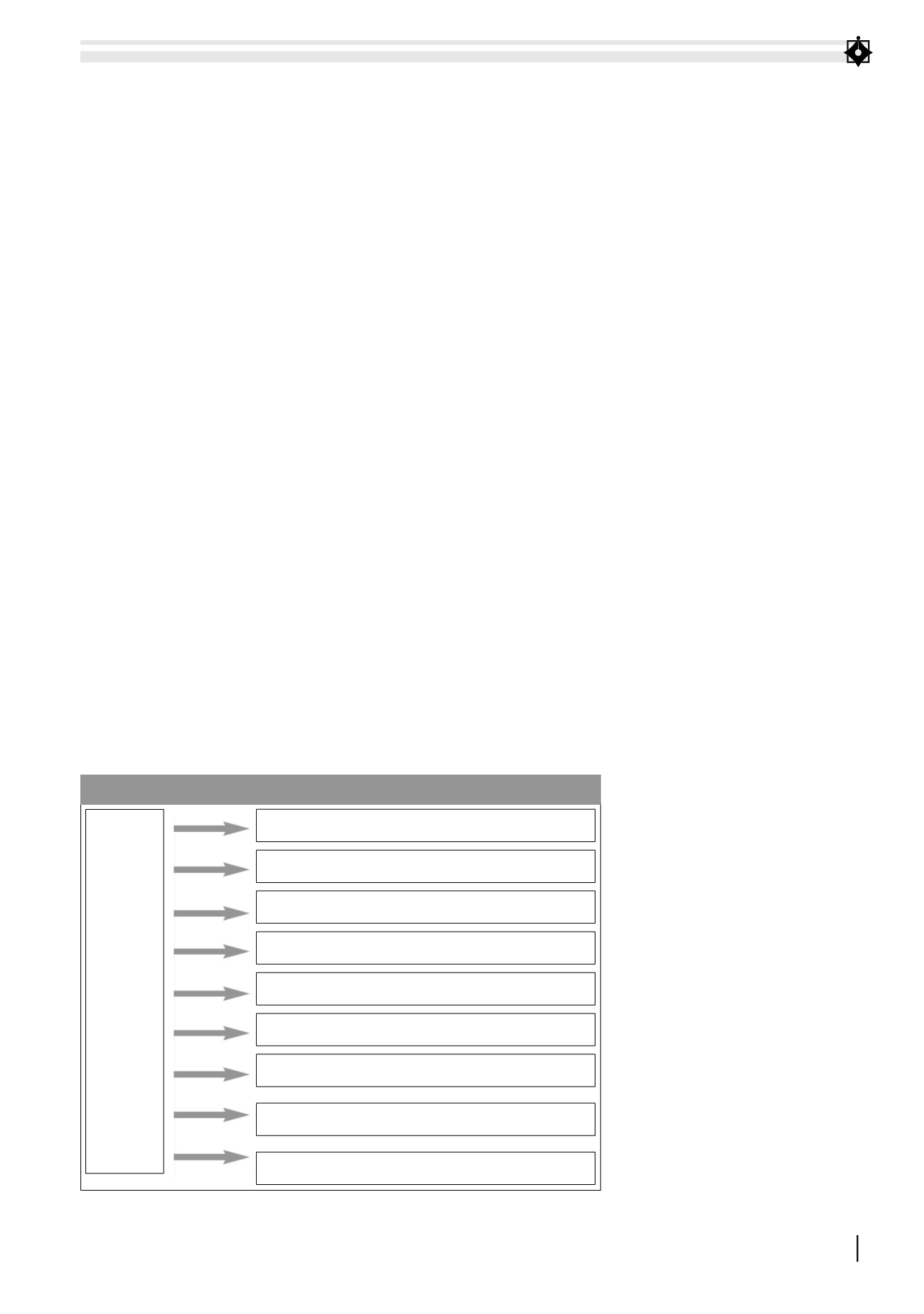

Step 1: Determine the target of the accounting system

Step 2: Identify the nancial responsibility center

Step 3: Build classi cation system

Step 4: Set up management accounting reports

Step 5: Select solution for management accounting

Step 6: Design voucher system, account for management accounting

Step 7: Set up estimation system

Step 8: Draft "Regulations on management accounting in enterprises"

Step 9: Make organizational changes

FIGURE 1: MODE OF DEVELOPING MANAGEMENT ACCOUNTING IN ENTERPRISES

Sorce: The authors collect